Navigating the world of investing is challenging enough without the added complexity of the tax code. However, understanding how your investments are taxed is not just a year-end chore—it’s a critical component of a successful, long-term wealth-building strategy. Missteps can lead to a significant and unnecessary drain on your returns, while strategic planning can legally minimize your tax burden and keep more of your hard-earned money working for you.

This guide provides a thorough examination of the two primary forms of investment taxation in the United States: Capital Gains and Dividends. We will demystify the terminology, explain the rules in plain English, and offer practical strategies to help you make more tax-efficient investment decisions. Our goal is to empower you with the knowledge to confidently manage your portfolio and engage effectively with financial professionals.

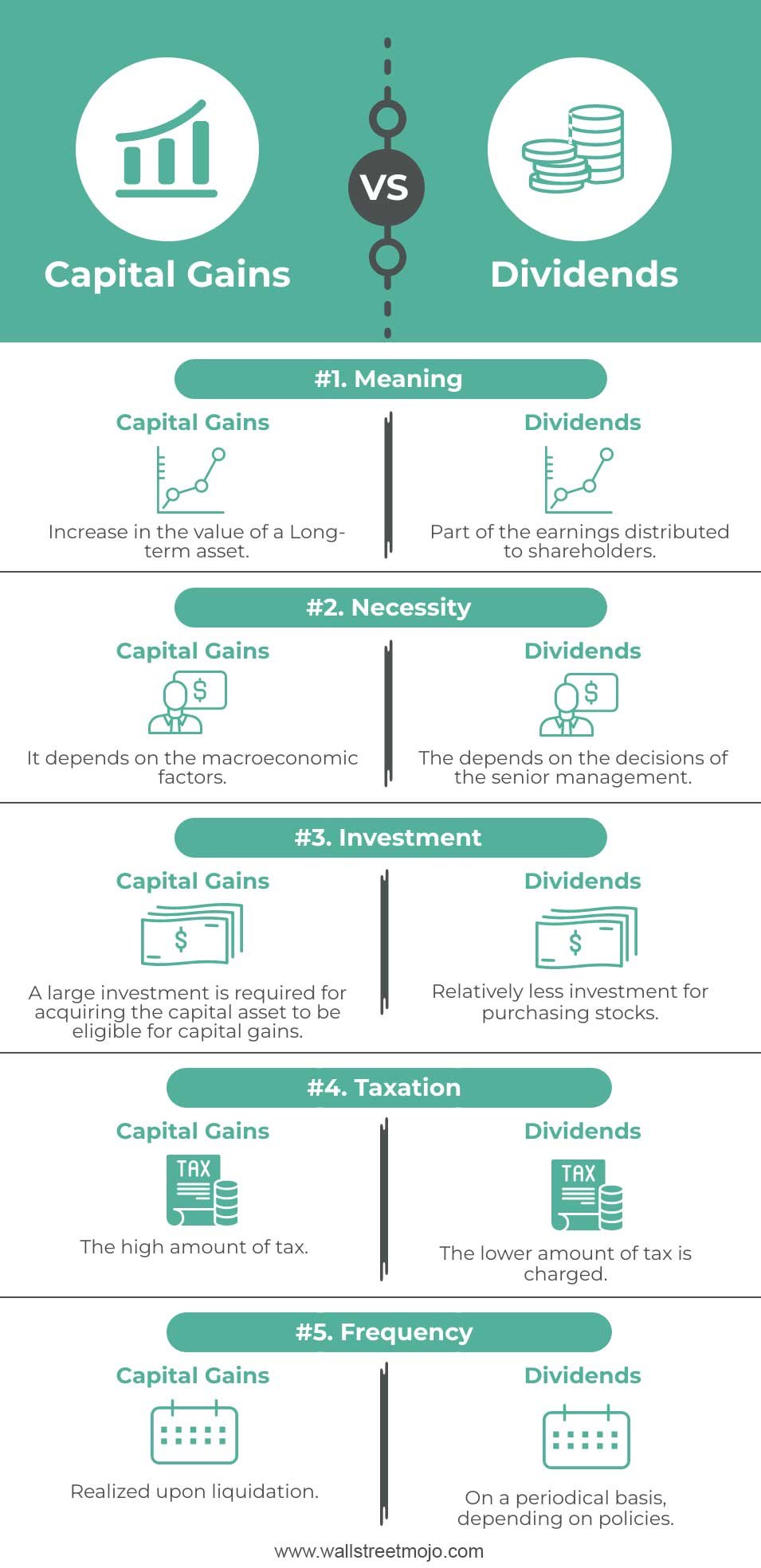

Part 1: Capital Gains Tax: The Tax on Profit

A capital gain is the profit you earn when you sell a capital asset for more than your original purchase price. Common capital assets include stocks, bonds, real estate (that isn’t your primary residence), and other investments.

- Capital Gain = Selling Price – Purchase Price (Cost Basis)

Conversely, a capital loss occurs when you sell an asset for less than your cost basis. These losses can be used to offset gains, a powerful tool we will discuss later.

The tax you pay on these profits is called the capital gains tax. The rate you pay is not a single, universal number. It is determined by two crucial factors:

- How long you held the asset before selling it (The Holding Period).

- Your taxable income for the year.

The Critical Distinction: Short-Term vs. Long-Term Capital Gains

The holding period is the most significant determinant of your tax rate. The line in the sand is one year.

Short-Term Capital Gains (STCG)

- Definition: Gains on assets held for one year or less.

- Taxation: These gains are taxed at your ordinary income tax rates. This is the same rate applied to your salary, wages, and other regular income. For most investors, this is the highest possible tax rate they will face, making it generally undesirable from a tax perspective.

2024 Federal Ordinary Income Tax Brackets (For Illustration)

| Tax Rate | For Single Filers | For Married Filing Jointly |

|---|---|---|

| 10% | Up to $11,600 | Up to $23,200 |

| 12% | $11,601 to $47,150 | $23,201 to $94,300 |

| 22% | $47,151 to $100,525 | $94,301 to $201,050 |

| 24% | $100,526 to $191,950 | $201,051 to $383,900 |

| 32% | $191,951 to $243,725 | $383,901 to $487,450 |

| 35% | $243,726 to $609,350 | $487,451 to $731,200 |

| 37% | Over $609,350 | Over $731,200 |

Source: IRS, 2024 figures adjusted for inflation.

If you are in the 24% tax bracket and realize a short-term gain, you will pay a 24% federal tax on that profit.

Long-Term Capital Gains (LTCG)

- Definition: Gains on assets held for more than one year.

- Taxation: These gains are taxed at preferential, lower rates. The long-term capital gains rates are 0%, 15%, or 20%, depending on your taxable income.

2024 Federal Long-Term Capital Gains Tax Brackets

| Tax Rate | For Single Filers | For Married Filing Jointly |

|---|---|---|

| 0% | Up to $47,025 | Up to $94,050 |

| 15% | $47,026 to $518,900 | $94,051 to $583,750 |

| 20% | Over $518,900 | Over $583,750 |

Source: IRS, 2024 figures adjusted for inflation.

Why This Distinction Matters: A Powerful Example

Let’s say you are a single filer with a taxable income of $90,000. You bought shares of XYZ Corp and are considering selling them for a $10,000 profit.

- Scenario A: You sell after 11 months (Short-Term Gain).

- Your $90,000 income plus the $10,000 gain puts you in the 24% ordinary income bracket for this profit.

- Tax Owed: $10,000 x 24% = $2,400

- Scenario B: You wait one more month and sell after 1 year and 11 months (Long-Term Gain).

- Your total taxable income is $100,000 ($90,000 + $10,000). Looking at the LTCG table, this falls within the 15% bracket for long-term gains.

- Tax Owed: $10,000 x 15% = $1,500

By simply holding the investment for over one year, you save $900 in federal taxes on this single transaction. This powerful incentive is designed to encourage long-term investing.

Calculating Your Cost Basis: The Foundation of the Calculation

Your cost basis is essentially your investment in the asset for tax purposes. It starts as the purchase price but can be adjusted over time.

- Initial Purchase: You buy 10 shares of ABC stock at $50 per share. Your cost basis is $500.

- Commissions/Fees: In the past, brokerage commissions were added to your basis. Today, most are $0, but if you pay any fees, they are included.

- Reinvested Dividends: If you automatically reinvest dividends, each reinvestment purchases new shares, each with its own cost basis and holding period.

- Splits and Mergers: Stock splits adjust your per-share basis. For example, a 2-for-1 split on your 10 shares at $50 would give you 20 shares with a $25 per-share basis.

Choosing a Cost Basis Method

If you buy shares of the same stock or fund at different times and prices, you will have multiple “lots.” When you sell only part of your holdings, you can choose which lots to sell. Common methods include:

- First-In, First-Out (FIFO): The oldest shares are sold first.

- Specific Identification: You specifically select which lots to sell. This offers the greatest tax flexibility.

Example of Specific Identification: You own three lots of XYZ Fund:

- 10 shares bought 2 years ago at $20/share.

- 10 shares bought 1.5 years ago at $30/share.

- 10 shares bought 3 months ago at $15/share.

You want to sell 10 shares today at $35/share. Using Specific ID, you can choose to sell Lot #3, realizing a short-term gain of $200 (($35-$15) x 10), or you could sell Lot #1, realizing a long-term gain of $150 (($35-$20) x 10). The strategic choice is clear.

The Net Investment Income Tax (NIIT)

High-income earners must be aware of an additional 3.8% tax. The Net Investment Income Tax applies to the lesser of:

- Your Net Investment Income (which includes capital gains and dividends), or

- Your Modified Adjusted Gross Income (MAGI) over certain thresholds ($200,000 for single filers, $250,000 for married filing jointly).

This tax is applied on top of the standard capital gains rates. For someone in the 20% LTCG bracket, the NIIT can make their effective top federal rate 23.8%.

Capital Losses: The Silver Lining

Realizing a loss is never fun, but the tax code provides a mechanism to use them to your advantage.

- Offsetting Gains: You must first use your capital losses to offset capital gains of the same type. Short-term losses offset short-term gains; long-term losses offset long-term gains.

- Netting Process: After matching ST vs. LT, if you have a net loss in one category, it can be used to offset a net gain in the other. For example, a net short-term loss can offset a net long-term gain.

- Deducting Against Ordinary Income: If your total net capital loss for the year exceeds your gains, you can deduct up to $3,000 ($1,500 if married filing separately) against your ordinary income (e.g., your salary).

- Carrying Forward Losses: Any remaining losses beyond the $3,000 limit can be carried forward indefinitely to future tax years, where they can offset future gains and income.

This is the principle behind Tax-Loss Harvesting—a strategic practice of selling securities at a loss to offset realized gains, thereby reducing your current tax bill.

Part 2: Dividend Tax: The Tax on Distributions

Dividends are payments made by a corporation to its shareholders, representing a portion of the company’s profits. They are a popular source of passive income for investors. However, not all dividends are created equal for tax purposes.

Types of Dividends: Ordinary vs. Qualified

Ordinary Dividends (Non-Qualified)

- What they are: These are the most common type of dividend and are paid from a company’s earnings and profits. They are also referred to as “non-qualified” dividends.

- Taxation: They are taxed at your ordinary income tax rates, just like short-term capital gains or your salary. This makes them the least tax-efficient form of dividend.

Qualified Dividends

- What they are: These are a subset of ordinary dividends that meet specific IRS criteria to receive preferential tax treatment.

- Criteria to be “Qualified”:

- The dividend must be paid by a U.S. corporation or a qualified foreign corporation.

- The dividends are not listed as non-qualifying (e.g., from certain credit unions, mutual insurance companies, etc.).

- You must have held the stock for a “minimum holding period.” This is the critical investor-controlled factor.

- For common stock: You must have held the shares for more than 60 days during the 121-day period that begins 60 days before the ex-dividend date.

- For preferred stock, it’s more than 90 days during the 181-day period starting 90 days before the ex-dividend date.

- Taxation: Qualified dividends are taxed at the favorable long-term capital gains tax rates (0%, 15%, or 20%).

Why This Distinction Matters: Another Example

You are a single filer with a taxable income of $90,000. You own two stocks:

- Stock A: Pays $1,000 in qualified dividends. You held it for the required period.

- Stock B: Pays $1,000 in ordinary dividends.

- Tax on Stock A (Qualified): $1,000 x 15% = $150

- Tax on Stock B (Ordinary): $1,000 x 22% (your marginal rate) = $220

By ensuring your dividends are “qualified,” you save $70 on just $1,000 of dividend income.

Special Types of Distributions

- Return of Capital (ROC): These are not considered dividends initially. They are a return of part of your original investment, which lowers your cost basis. You don’t pay tax on ROC immediately, but a lower basis means a higher capital gain (or lower loss) when you eventually sell the asset. Real Estate Investment Trusts (REITs) often make ROC distributions.

- Capital Gains Distributions from Mutual Funds/ETFs: When a fund manager sells holdings within the fund for a profit, they are required to distribute those net capital gains to shareholders. These distributions are classified as long-term capital gains on your Form 1099-DIV, regardless of how long you have held the fund shares, and are taxed at the LTCG rates.

Read more: Navigating the Supply Chain: A 2024 Analysis of U.S. Logistics and Infrastructure

Part 3: Advanced Topics and Tax-Efficient Investing Strategies

Understanding the rules is the first step; applying them strategically is the next.

1. The Power of Tax-Advantaged Accounts

The simplest way to manage investment taxes is to avoid them altogether until retirement by using tax-advantaged accounts.

- Traditional IRA/401(k): Contributions may be tax-deductible. Investments grow tax-deferred. You pay ordinary income tax on all withdrawals in retirement. There are no capital gains or dividend taxes during the accumulation phase.

- Roth IRA/Roth 401(k): Contributions are made with after-tax money. The key benefit: investments grow completely tax-free. Qualified withdrawals in retirement, including all gains, are entirely free from federal income tax.

- Health Savings Account (HSA): If you have a high-deductible health plan, HSAs offer the ultimate triple tax advantage: contributions are tax-deductible, growth is tax-deferred, and withdrawals for qualified medical expenses are tax-free.

Strategic Placement: Hold investments that generate frequent short-term trades, high yields of non-qualified dividends (like REITs), or taxable bond interest inside tax-advantaged accounts. Hold long-term buy-and-hold investments that generate qualified dividends and long-term capital gains in taxable brokerage accounts.

2. Tax-Loss Harvesting in Depth

This is the practice of selling an investment that has decreased in value to realize a capital loss. You then use that loss to offset realized capital gains or up to $3,000 of ordinary income.

- The “Wash Sale” Rule: The IRS prevents you from claiming a loss if you buy a “substantially identical” security 30 days before or after the sale. You cannot simply sell a stock for a loss and immediately buy it back.

- Strategy: To stay invested, you can immediately use the sale proceeds to purchase a different but similar investment. For example, sell an S&P 500 ETF (like IVV) at a loss and simultaneously buy a different S&P 500 ETF (like VOO). This maintains your market exposure while realizing the tax loss.

3. Holding Period Management

Be acutely aware of the one-year mark for capital gains and the 60-day rule for qualified dividends. A single day can mean the difference between a 15% and a 37% tax rate on a gain. Avoid triggering short-term gains unless there is a compelling, non-tax reason to do so.

4. Gifting Appreciated Stock

Instead of gifting cash to family members in lower tax brackets, consider gifting appreciated stock. The recipient receives the stock with your original cost basis and holding period. If they are in the 0% long-term capital gains bracket, they can sell the stock and potentially pay zero federal tax on the appreciation that occurred while you owned it. This is a powerful wealth-transfer strategy.

5. Understanding State Taxes

Do not forget state-level taxation! The federal government provides preferential rates for long-term gains and qualified dividends, but most states do not. They typically tax all investment income as ordinary income at the state’s income tax rate. This can add a significant additional layer of tax, especially for residents of high-tax states like California, New York, or New Jersey.

Part 4: Practical Guide and Reporting

Key Tax Forms

- Form 1099-B: Sent by your broker, it reports proceeds from broker transactions (sales of stocks, bonds, etc.). It details the sale date, proceeds, and cost basis.

- Form 1099-DIV: Reports dividends and distributions you received during the year, breaking them out into Ordinary Dividends, Qualified Dividends, and Capital Gains Distributions.

- Form 1099-INT: Reports interest income (e.g., from bonds or savings accounts).

- Schedule D (Form 1040): This is the form you use to report all your capital gains and losses, calculated from the 1099-Bs.

- Form 8949: Used to report the details of each individual sale, which are then summarized on Schedule D.

The Importance of Record Keeping

Maintain your own records of trades, cost basis, and holding periods. While brokers are required to track cost basis for most securities, errors can happen, and older “non-covered” shares may not be tracked. Your own records are your best defense in an audit.

Read more: Beyond Silicon Valley: Mapping the USA’s Emerging Tech Hubs and Investment Hotspots

Conclusion: Knowledge is Power (and Savings)

Taxes on investments are an inevitable part of building wealth, but they don’t have to be an overwhelming burden. By understanding the fundamental difference between short-term and long-term capital gains, and between ordinary and qualified dividends, you can make informed decisions that significantly enhance your after-tax returns.

The core principles are simple: favor long-term holdings over short-term trading, utilize tax-advantaged accounts to their fullest, and strategically use losses to offset gains. While this guide provides a comprehensive foundation, every investor’s situation is unique. Consulting with a qualified CPA or certified financial planner (CFP®) can provide personalized advice tailored to your specific financial goals and tax circumstances. By being proactive and knowledgeable, you can ensure the tax code works for you, not against you.

Frequently Asked Questions (FAQ)

1. I bought and sold a stock within the same year. How is it taxed?

This is a short-term capital gain (or loss). The profit will be added to your ordinary income (like your salary) and taxed at your marginal federal income tax rate, which can be as high as 37%. You will not receive the beneficial long-term capital gains rate.

2. What is the “cost basis” of an inherited stock?

When you inherit a stock or other asset, you generally receive a “step-up in basis.” This means your cost basis is reset to the fair market value of the asset on the date of the original owner’s death. This is a massive tax advantage, as it effectively erases all the capital gains that accrued during the deceased’s lifetime. When you sell the inherited asset, you only pay tax on the appreciation from the value at the date of death.

3. How are investments in my Roth IRA taxed?

The growth and withdrawals within a Roth IRA are tax-free, provided you are at least 59½ and have held the account for at least five years. There are no taxes on dividends, capital gains, or interest earned inside the account. You can buy and sell investments within the Roth IRA without any tax consequences.

4. What is a “wash sale” and why does it matter?

A wash sale is a rule that disallows a tax loss claim if you sell a security at a loss and repurchase a “substantially identical” security within 30 days before or after the sale. The disallowed loss is added to the cost basis of the newly purchased shares, effectively deferring the loss until you eventually sell the new shares. This rule is crucial to understand for tax-loss harvesting strategies.

5. I have a net capital loss of $10,000 this year. What happens?

You will first use the loss to offset any capital gains you have (if any). Then, you can deduct up to $3,000 of the remaining loss against your ordinary income (e.g., your wages). The remaining $7,000 loss is not wasted; it can be carried forward to future tax years indefinitely. Next year, you can use this $7,000 to offset future gains and another $3,000 of ordinary income.

6. Are there any investments that are completely tax-free?

Yes. The interest earned on municipal bonds (“munis”) is generally exempt from federal income tax. If you buy munis issued by your state of residence, the interest is also typically exempt from state and local taxes. However, capital gains from selling a municipal bond are still taxable.

7. My mutual fund didn’t pay me anything, but I got a tax form showing capital gains. Why?

Mutual funds are required to distribute their net realized capital gains to shareholders at least once a year. Even if you didn’t sell any of your fund shares, you are still responsible for paying taxes on your proportionate share of the gains the fund manager realized by selling stocks within the fund’s portfolio. This is a key reason to be aware of a fund’s “turnover ratio” before investing in a taxable account.

8. How can I find out if my dividends are “qualified”?

Your brokerage will send you a Form 1099-DIV after the end of the year. Box 1a shows “Total Ordinary Dividends,” and the crucial Box 1b shows “Qualified Dividends.” The amount in Box 1b is what gets the preferential tax rate. It is your responsibility to ensure you met the holding period requirement for those shares.