Summary

The Federal Reserve (the Fed) wields extraordinary influence over U.S. market performance through its monetary policy decisions. By adjusting interest rates, managing liquidity, and signaling future actions, the Fed shapes investor behavior, credit costs, and overall economic growth. Understanding the Fed’s role is essential for anyone navigating the complex world of U.S. equities, bonds, and financial markets.

1. Understanding the Federal Reserve’s Mandate and Power

What is the Federal Reserve’s mission?

The U.S. Federal Reserve has a dual mandate assigned by Congress:

- Promote maximum sustainable employment, and

- Maintain stable prices (inflation control).

Beyond these, it aims for moderate long-term interest rates and overall financial stability. This dual responsibility makes the Fed the single most powerful financial institution in the world, with decisions that ripple across global markets.

Who decides monetary policy?

Monetary policy decisions are made by the Federal Open Market Committee (FOMC) — a group consisting of seven members from the Board of Governors and five of the twelve regional Federal Reserve Bank presidents. The FOMC meets eight times annually (and more if needed) to determine whether to tighten, ease, or maintain monetary policy settings.

The Fed’s Primary Tools

The Federal Reserve controls monetary policy using a variety of tools, each of which can directly or indirectly affect U.S. financial markets:

- Federal Funds Rate (Interest Rate Policy):

This is the interest rate banks charge each other for overnight loans. It serves as a benchmark for other interest rates in the economy, including mortgages, auto loans, and corporate debt. - Open Market Operations (OMO):

The Fed buys or sells U.S. Treasury securities in the open market to influence liquidity and short-term interest rates. - Quantitative Easing (QE) and Tightening (QT):

QE involves large-scale asset purchases (Treasuries, MBS) to lower long-term interest rates and stimulate investment. QT reverses this process, reducing the money supply. - Discount Rate and Reserve Requirements:

The discount rate is what banks pay to borrow directly from the Fed, while reserve requirements dictate how much capital banks must hold, affecting lending capacity. - Forward Guidance and Communication:

The Fed influences market expectations by signaling its future intentions through press conferences, reports, and FOMC statements.

Each tool acts as a lever, allowing the Fed to cool or stimulate the economy depending on inflation, growth, and employment data.

2. How the Fed’s Actions Transmit Through the Market

The Fed’s policy decisions don’t just impact interest rates—they shape behavior, expectations, and asset valuations across multiple channels.

Let’s break down these transmission mechanisms:

2.1 Interest Rate Channel

When the Fed raises or lowers the federal funds rate:

- Borrowing costs for households and businesses change.

- Consumer spending, mortgage rates, and corporate investment decisions adjust.

- A lower rate stimulates the economy; a higher rate cools it.

- These shifts ultimately affect company earnings, investor confidence, and stock prices.

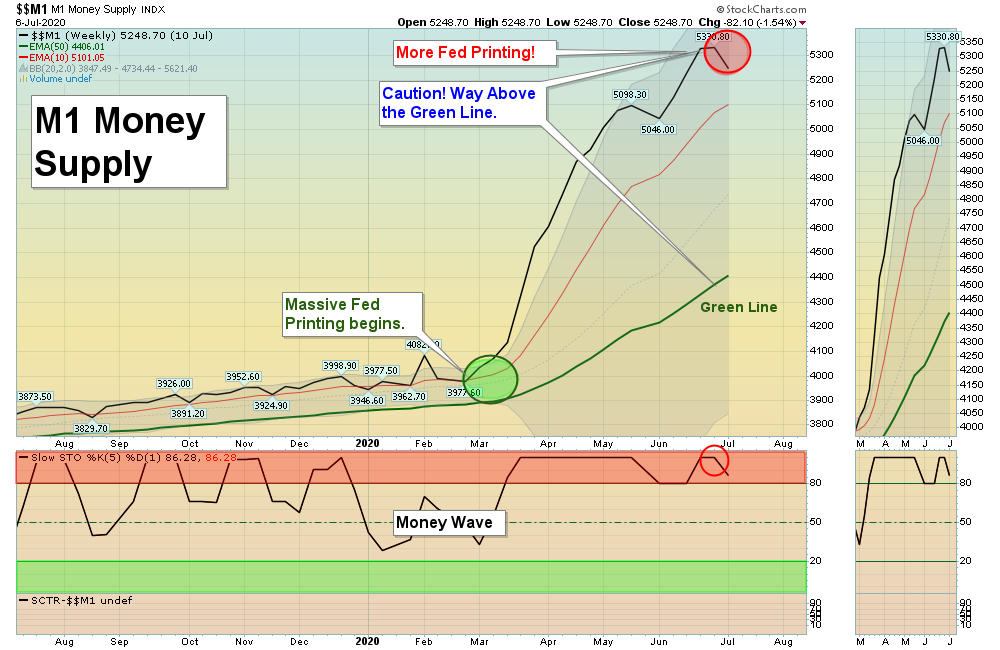

For example, during 2020, the Fed slashed rates to near zero amid the pandemic, which made borrowing cheaper, boosted risk-taking, and ignited a historic rally in equities.

2.2 Valuation / Discounting Channel

Interest rates serve as the discount rate for valuing future cash flows.

- Higher rates = higher discount rate = lower present value.

- Growth stocks (like tech firms) with profits far in the future tend to fall more during rate hikes.

- Conversely, when rates are low, valuations expand as investors pay more for future growth.

2.3 Credit and Risk Premium Channel

Fed policy affects the cost and availability of credit:

- Tightening increases risk premiums, widening spreads between corporate bonds and Treasuries.

- Easing reduces those spreads, making borrowing easier for corporations and consumers.

This channel is crucial for the housing, auto, and credit card markets.

2.4 Wealth and Portfolio Rebalancing Channel

When interest rates decline, bond yields drop, pushing investors toward equities and other riskier assets seeking better returns.

When rates rise, money flows back into safer fixed-income assets.

This rotation affects asset classes differently:

- Rate cuts → Equities, real estate, and commodities rally.

- Rate hikes → Defensive sectors and bonds gain relative attractiveness.

2.5 Expectations & Signaling Channel

The Fed’s communication strategy—its press conferences, statements, and “dot plots”—sets market tone.

- A hawkish signal (hinting at rate hikes) can trigger immediate selloffs.

- A dovish signal (hinting at cuts) can cause a relief rally.

Sometimes, what the Fed says moves markets more than what it does.

3. Asset Class Breakdown: How the Fed Affects Different Markets

3.1 Stock Market Impacts

The stock market often responds to Fed policy faster than the economy.

When the Fed cuts rates:

- Borrowing costs drop.

- Corporate earnings improve.

- Investors are more willing to take risks.

- The stock market usually rallies.

When the Fed raises rates:

- Higher discount rates lower valuations.

- Growth sectors (especially tech) take a hit.

- Defensive sectors—utilities, healthcare, and consumer staples—outperform.

Sector Rotation Example:

- Rising rates → Financials benefit (banks earn higher interest margins).

- Falling rates → Growth sectors and real estate outperform.

The “Fed effect” can be seen in major market shifts:

- The 2022 tightening cycle crushed high-growth stocks and speculative tech names.

- The 2024 pivot toward rate cuts revived the S&P 500, especially small-cap and cyclical stocks.

3.2 Bond and Fixed-Income Markets

The bond market’s relationship with the Fed is even more direct.

- When the Fed hikes, short-term Treasury yields rise.

- But long-term yields may not always follow—depending on inflation expectations and investor confidence.

For example:

- In 2023–24, while the Fed raised rates, the long-term yield curve inverted, signaling market expectations of slower growth or a future recession.

- During QE programs (2009–2021), long-term yields fell sharply, supporting borrowing and asset prices.

Corporate Bonds:

- In tightening cycles, credit spreads widen (riskier borrowers pay more).

- In easing cycles, spreads compress (cheaper refinancing and stronger corporate balance sheets).

3.3 Currency and Global Capital Flows

The Fed’s rate decisions influence global capital movement and the U.S. dollar’s strength.

- Higher U.S. rates attract global investors → Dollar appreciates.

- Lower U.S. rates encourage capital outflow → Dollar weakens.

This has direct implications for:

- Exporters: A strong dollar makes U.S. goods less competitive abroad.

- Commodities: Since commodities are priced in USD, a stronger dollar often pushes their prices down.

- Emerging markets: Rising U.S. rates can cause capital flight from emerging economies, tightening their financial conditions.

3.4 Real Estate and Credit Markets

The housing market is extremely sensitive to interest rates.

- When the Fed raises rates, mortgage rates increase, reducing affordability.

- When the Fed cuts rates, mortgages become cheaper, boosting home demand and construction activity.

For instance, the Fed’s rate hikes in 2022–23 pushed the average 30-year mortgage rate above 7%, the highest in two decades, cooling home prices and construction starts.

4. Real-World Examples of Fed Impact

2004–2006 Tightening Cycle

The Fed gradually raised rates from 1% to 5.25%.

Initially, markets remained strong, but rising mortgage rates triggered stress in housing—a prelude to the 2008 crisis.

2008–2009 Financial Crisis

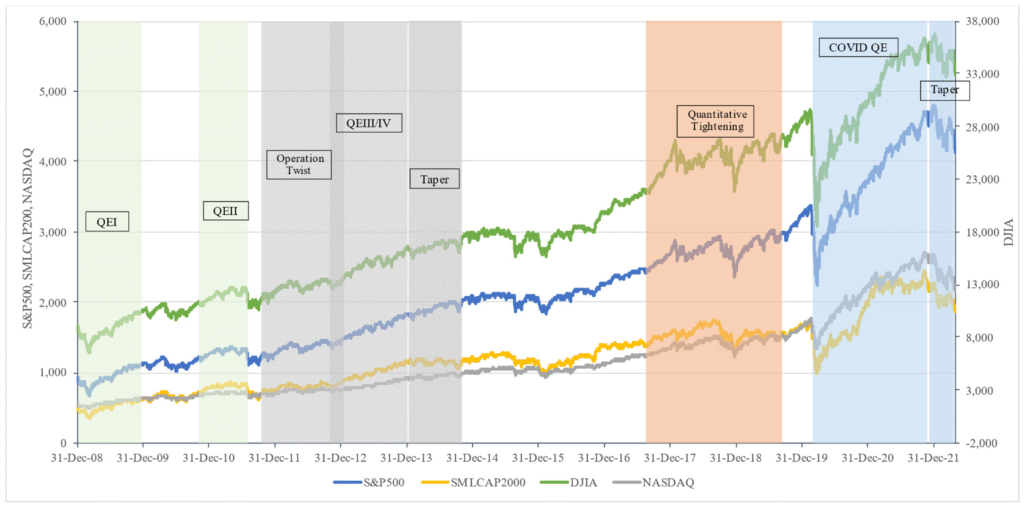

The Fed cut rates to near zero and launched quantitative easing (QE) for the first time.

QE restored liquidity, lowered borrowing costs, and eventually helped markets recover, although not without creating long-term distortions.

2013 “Taper Tantrum”

When the Fed hinted at reducing QE, bond yields spiked and emerging markets sold off sharply. This episode highlighted how even verbal guidance can trigger global volatility.

2020 Pandemic Response

Facing a global shutdown, the Fed cut rates to zero, initiated unlimited QE, and provided liquidity facilities to stabilize markets.

This intervention supported the fastest post-crisis market rebound in modern history.

2022–2024 Aggressive Tightening and Pivot

To combat inflation, the Fed raised rates from near-zero to over 5% in record time. The move pressured tech valuations and triggered volatility in banking and real estate sectors.

By late 2024, as inflation moderated, the Fed signaled rate cuts for 2025—fueling optimism and a resurgence in risk assets.

5. Challenges and Market Complexities

5.1 The Lag Effect

The Fed’s policies take time—often 6 to 18 months—to fully influence the economy.

Investors frequently underestimate these “long and variable lags,” leading to premature reactions or mispricing.

5.2 Market Anticipation

Markets often price in future Fed moves.

If traders expect a rate hike, asset prices may adjust weeks before the official decision.

This is why surprises—unexpectedly hawkish or dovish announcements—create outsized volatility.

5.3 Global and Fiscal Factors

Not everything is under the Fed’s control.

- Geopolitical shocks

- Supply chain disruptions

- U.S. fiscal deficits

- Commodity price swings

can all distort monetary policy effectiveness.

5.4 The “Fed Put” Problem

Many investors believe the Fed will always rescue markets during downturns.

This belief—called the “Fed Put”—encourages excessive risk-taking.

But it’s risky to assume perpetual support; policy credibility matters more than short-term rallies.

6. FAQs: What Americans Are Asking About the Fed

Q1. How does the Federal Reserve affect the stock market?

By changing interest rates and liquidity, the Fed alters corporate borrowing costs, earnings projections, and investor risk appetite.

Q2. What is the federal funds rate?

It’s the short-term rate banks charge each other overnight. It influences nearly all other interest rates, from mortgages to credit cards.

Q3. Do rate cuts always boost stocks?

No. If rate cuts signal economic trouble, they may initially hurt confidence even though they support growth longer term.

Q4. Why do bond yields rise even after rate cuts?

Investors might expect higher inflation or large government deficits, which push long-term yields up despite short-term easing.

Q5. What is quantitative easing (QE)?

QE is the Fed’s program of buying long-term securities to inject liquidity, lower yields, and stimulate lending.

Q6. How long does it take for rate changes to affect the economy?

Usually between 6 and 18 months, depending on the speed of credit transmission and consumer response.

Q7. Does the Fed control inflation completely?

Not entirely. It influences demand-side factors, but supply shocks (like energy prices) can limit its control.

Q8. Why do investors track the Fed’s dot plot?

The “dot plot” shows each FOMC member’s rate expectations—giving clues about the future path of policy.

Q9. How do Fed actions affect credit spreads?

Rate hikes widen spreads (higher risk premiums), while cuts compress them, making borrowing cheaper.

Q10. What happens if the Fed loses credibility?

Markets become volatile. Inflation expectations may become unanchored, and interest rates could rise uncontrollably.

7. Practical Investor Takeaways

Key Lessons

- Watch the Fed’s tone, not just the numbers.

A single phrase in a press conference can move markets more than the rate decision itself. - Follow the yield curve.

Inverted curves (short rates above long rates) often precede recessions. - Adapt your portfolio to the rate cycle.

- During rate hikes: focus on defensive stocks, financials, and shorter-duration bonds.

- During rate cuts: growth stocks, small caps, and real estate typically outperform.

- Manage risk and avoid overreliance.

Don’t assume the Fed will always “bail out” the market; use hedges like TIPS, gold, or diversified ETFs. - Diversify geographically.

U.S. rate moves ripple globally—emerging markets, commodities, and currencies react differently. - Stay data-driven.

Watch inflation reports, job data, and FOMC minutes. They often foreshadow the next Fed move.

8. The Future of Fed Policy and Market Outlook (2025–2030)

As of late 2025, the Fed is walking a fine line.

- Inflation has cooled from its pandemic-era highs.

- Employment remains steady but softening.

- Fiscal deficits are pressuring long-term yields.

Analysts expect gradual rate cuts through 2026—but not a full return to zero interest rates.

Long-term implications:

- U.S. markets may see lower volatility compared to 2022–23, but real yields could remain elevated.

- Investors should prepare for a world where Fed policy is less about emergency intervention and more about normalization.

In the coming decade, technology-driven productivity, AI adoption, and demographic shifts will also influence how the Fed calibrates policy.

Ultimately, while the Federal Reserve shapes the playing field, markets will continue to interpret, anticipate, and sometimes defy its every move.

Read this also : https://fazi.world/category/market-analysis/