Imagine two neighbors, Alex and Taylor. They both earn the same salary, save the same amount for retirement each year, and retire with identical $1.5 million portfolios. Yet, in retirement, Alex has significantly more spendable, after-tax income than Taylor. How is this possible?

The difference wasn’t luck or investment genius. It was a single, foundational decision made decades earlier: the choice between a Roth and a Traditional retirement account.

This is arguably the most consequential tax decision the average American investor will make. It’s a choice between a tax break today versus a tax break tomorrow—a decision that hinges on predicting your future financial life in an uncertain world.

This guide will demystify this critical choice. We will move beyond oversimplified rules of thumb and dive deep into the mechanics, the math, and the strategic considerations. By the end, you will have a clear framework to determine which account—or what blend of both—is the right tool to build a tax-efficient retirement.

Part 1: The Core Mechanics – Two Different Tax Vehicles

Before we can compare, we must understand how each account works on a fundamental level.

The Traditional Account: The “Deferral” Model

The Analogy: Think of a Traditional 401(k) or IRA as a tax-free greenhouse. You are given a seed (your income) and the government says, “You don’t have to pay tax on that seed if you plant it in this greenhouse.” The seed grows into a large tree (your investments grow) entirely protected from current taxes. However, when you eventually go to pick the fruit (withdraw money in retirement), you must pay income tax on every piece of fruit you harvest.

The Mechanics:

- Contributions: Made with pre-tax dollars. This directly reduces your Adjusted Gross Income (AGI) for the year you contribute. For example, if you earn $60,000 and contribute $10,000 to a Traditional 401(k), your taxable income for that year falls to $50,000.

- Growth: All investment gains—dividends, interest, and capital appreciation—accumulate tax-deferred. You pay no taxes on this growth year after year.

- Withdrawals: In retirement, every dollar you withdraw is treated as ordinary income and taxed at your marginal income tax rate at that time.

The Immediate Benefit: The upfront tax deduction. This lowers your current tax bill, effectively giving you a government subsidy for saving.

The Roth Account: The “Pay Now, Save Later” Model

The Analogy: Think of a Roth IRA or Roth 401(k) as a tax-free fortress. You start with a seed, but you must pay the tax on it upfront before you can bring it inside the fortress walls. Once inside, the seed grows into a massive tree, completely shielded from any further taxes. When you retire, you can harvest all the fruit you want, forever tax-free.

The Mechanics:

- Contributions: Made with after-tax dollars. You get no tax deduction in the year you contribute. Using the same example, if you earn $60,000 and contribute to a Roth, you still pay income tax on the full $60,000.

- Growth: All investment gains accumulate tax-free.

- Withdrawals: In retirement, qualified withdrawals are 100% tax-free. This includes both your original contributions and all the growth they’ve generated. To be qualified, the distribution must occur after age 59½ and the account must have been open for at least five years.

The Long-Term Benefit: Tax-free growth and withdrawals. You eliminate future tax liability on this portion of your wealth.

Part 2: The Fundamental Question: Tax Rates Now vs. Then

The classic, mathematical argument for choosing between Roth and Traditional boils down to a single comparison:

Will your marginal tax rate in retirement be higher or lower than it is today?

- If you expect your tax rate in retirement to be LOWER than it is today → Choose TRADITIONAL. You take the deduction now at your high rate and pay taxes later at your lower rate. This is the winning financial move.

- If you expect your tax rate in retirement to be HIGHER than it is today → Choose ROTH. You pay taxes now at your low rate and enjoy tax-free withdrawals later when rates are high. This is the winning financial move.

It sounds simple. The problem, of course, is that predicting your tax rate 30 years from now is impossible. You must make an educated guess based on your career trajectory, future tax law changes, and retirement income needs.

Who Typically Benefits from a Traditional Account?

- High Earners in Their Peak Earning Years: If you are in the 32% or 35% federal tax bracket today, that upfront deduction is incredibly valuable. It’s likely that your taxable income (and thus your tax rate) will be lower in retirement.

- Those Nearing Retirement: If you are a few years out and at your highest lifetime earnings, the Traditional deduction shields a significant amount of income from high taxes.

- People Who Will Have a Much Lower Expenses in Retirement: If you plan to have your mortgage paid off and live a more modest lifestyle, your taxable income may naturally fall into a lower bracket.

Who Typically Benefits from a Roth Account?

- Young People and Early-Career Professionals: If you’re in the 12% or 22% bracket now and expect your income (and tax rate) to rise throughout your career, locking in today’s low rates with a Roth is a strategic masterstroke.

- Those Who Believe Tax Rates Will Rise in the Future: Given the U.S. national debt, many experts believe income tax rates may be higher across the board in the future. A Roth is a hedge against this risk.

- High Earners Who Max Out Contributions: If you’re maxing out your 401(k) ($23,000 in 2024), a Roth effectively allows you to save more. Why? Because $23,000 in a Roth is after-tax money, which is more valuable than $23,000 in a Traditional account that still has a tax liability attached. You’re stuffing more after-tax wealth into the tax-protected wrapper.

- Anyone Who Wants to Avoid RMDs: Traditional IRAs and 401(k)s are subject to Required Minimum Distributions (RMDs) starting at age 73. This forces you to withdraw money you may not need, increasing your taxable income. Roth IRAs have no RMDs, allowing the money to grow tax-free for your entire life and be passed on to heirs.

Part 3: Beyond the Math – Key Strategic Considerations

The “now vs. then” tax rate question is the core, but several other critical factors can sway the decision.

1. The Impact of an Employer Match

Rule #1: Always contribute enough to your 401(k) to get the full employer match, regardless of Roth or Traditional.

This is non-negotiable. An employer match is free money and an instant 100% return on your investment. It’s the most powerful wealth-building tool available to most people. Note: Employer matches are always made on a pre-tax basis into a Traditional 401(k) account, even if your contributions go to a Roth. This means most people will have a mix of both types of money in retirement, which is a good thing.

2. The Power of Contribution Limits

Let’s illustrate the “you can save more” concept with a simple example. Assume you are in the 24% tax bracket and can afford to invest $1,000 of your pre-tax income.

- Traditional 401(k): You put the full $1,000 into the account.

- Roth 401(k): To get $1,000 into the Roth, you must pay $240 in taxes first (24% of $1,000). So, it “costs” you more upfront to contribute the same nominal amount.

However, since the IRS contribution limit is the same for both ($23,000), by using the Roth, you are effectively stuffing more after-tax value into the same container. When you withdraw the money tax-free, you keep 100% of that $23,000 plus all its growth. With the Traditional, you’ll share a significant portion of that final balance with the government.

Read more: Beyond Silicon Valley: An Analysis of Emerging Tech Hubs and Talent Pools Across the United States

3. The Critical Difference in Withdrawal Rules & Flexibility

This is a massive, often-overlooked advantage for the Roth.

- Access to Contributions: You can withdraw your contributions (but not earnings) from a Roth IRA at any time, for any reason, without tax or penalty. This makes a Roth IRA a powerful, secondary emergency fund and provides a level of liquidity that Traditional accounts completely lack.

- No RMDs: As mentioned, the absence of Required Minimum Distributions for Roth IRAs provides immense flexibility. It allows your money to continue growing tax-free indefinitely, which is fantastic for estate planning and for retirees who don’t need the extra income.

4. The Value of Tax Diversification

You don’t have to choose just one. In fact, having a mix of Roth, Traditional, and taxable brokerage accounts is the ultimate strategic position.

Why Diversification is King:

In retirement, having both types of accounts gives you a “tax dial” you can turn each year.

- Need to make a large, one-time purchase (a new roof, a dream vacation)? Withdraw from your Roth account tax-free, which won’t push you into a higher tax bracket.

- Having a low-income year? Take withdrawals from your Traditional IRA to fill up the lower tax brackets (e.g., the 0% standard deduction and 10%, 12% brackets) in a tax-efficient manner.

This control over your taxable income is incredibly valuable and can save you tens of thousands of dollars over a 30-year retirement.

Part 4: Actionable Guidelines by Life Stage

Your optimal Roth/Traditional mix will evolve throughout your life. Here’s a stage-by-stage guide.

In Your 20s and Early 30s: The Roth Decade

- Default Recommendation: Prioritize Roth contributions (Roth IRA and/or Roth 401(k)).

- Why: You are likely in the lowest tax bracket of your career. Your income (and tax rate) has almost nowhere to go but up. Paying taxes now at 12% or 22% is a fantastic deal. The decades of tax-free growth you will get are almost unimaginably valuable.

In Your Mid-Career (40s-50s): The Hybrid Approach

- Default Recommendation: A deliberate mix of Traditional and Roth.

- Why: You are likely in your peak earning years, making Traditional deductions very attractive. However, you also have a clear enough view of retirement to start building your tax-free bucket.

- Strategy: Continue getting any employer match (which goes into Traditional). If you are in a very high tax bracket (32%+), making pre-tax Traditional contributions to lower your AGI is wise. Then, if you have more to save, fund a Roth IRA (via the Backdoor method if income is too high) to build your tax-free pool.

Nearing Retirement (5-10 Years Out): The Fine-Tuning Phase

- Default Recommendation: Analyze your projected retirement income and tax brackets.

- Why: You now have a much better idea of your future Traditional account RMDs and Social Security income.

- Strategy: If you discover your RMDs will push you into a high tax bracket, consider making Roth contributions now or executing Roth conversions—converting portions of your Traditional IRA to a Roth IRA during lower-income years and paying the taxes upfront. This can significantly reduce future RMDs.

In Retirement: The Distribution Phase

- Default Recommendation: Withdraw strategically from your different “buckets.”

- Why: To minimize your lifetime tax bill.

- Strategy: Use Traditional withdrawals to “fill up” your standard deduction and lower tax brackets each year. Use Roth withdrawals for any expenses beyond that, or for large, unexpected costs, to avoid being pushed into a higher tax bracket.

Part 5: Navigating the Nitty-Gritty: Rules and Limits

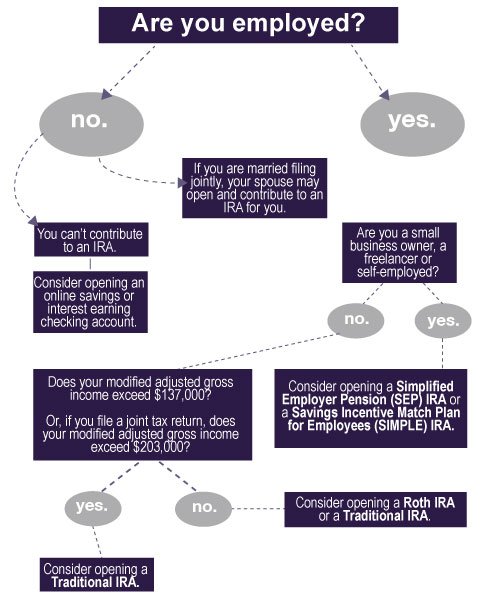

Income Limits (2024)

- Roth IRA: Eligibility to contribute phases out at higher incomes.

- Single/Head of Household: $146,000 – $161,000 MAGI

- Married Filing Jointly: $230,000 – $240,000 MAGI

- Traditional IRA: Anyone can contribute. However, the ability to deduct those contributions if you are covered by a workplace retirement plan phases out.

- Single/Covered by Plan: $77,000 – $87,000 MAGI

- Married/Joint/Covered by Plan: $123,000 – $143,000 MAGI

- Roth and Traditional 401(k): No income limits. Anyone with access to a workplace plan can contribute, regardless of how high their income is.

Read more: Digital Detox: 5 Science-Backed Techniques to Unplug and Reclaim Your Calm

The Backdoor Roth IRA Strategy

This is a legal, IRS-approved method for high earners (above the Roth IRA income limits) to get money into a Roth IRA.

- Make a non-deductible contribution to a Traditional IRA (which has no income limits).

- Shortly after, convert that Traditional IRA balance to a Roth IRA.

- Since you made the contribution with after-tax money and had no earnings, the conversion is tax-free.

Warning: This strategy gets complicated if you have other pre-tax IRA money (from rollovers or deductible contributions) due to the “pro-rata rule.” Consult a professional if this is the case.

Frequently Asked Questions (FAQ)

Q1: I really can’t predict my future tax rate. What should I do?

A: When in doubt, diversify. Splitting your contributions between Roth and Traditional is a perfectly sound and prudent strategy. It’s an admission that the future is uncertain and a way to hedge your bets. Having both types of accounts ready to use in retirement is far more important than picking the “perfect” one today.

Q2: Is it true that a Roth is always better for young people?

A: It is a very strong default recommendation, but not an absolute rule. A young person with significant student loan debt or a very low income might benefit more from the immediate tax refund provided by a Traditional contribution, which they could use to pay down high-interest debt. However, for most young people with a stable financial footing, the Roth’s decades of tax-free growth are unbeatable.

Q3: What if I need to retire early?

A: This is where the Roth’s flexibility shines. Since you can access your contributions anytime, a Roth IRA can be a crucial source of funding in early retirement before you can tap other retirement accounts without penalty. Strategies like Roth conversion ladders also use Roth accounts as a key tool for early retirees.

Q4: I’m in a high tax state but plan to retire in a state with no income tax. Does this change things?

A: Absolutely, and significantly. This is a strong point in favor of Traditional contributions. You get a deduction now against your high state and federal tax rate. In retirement, you will pay only federal income tax on those withdrawals, and at a potentially lower federal bracket. The state tax savings alone can make the Traditional route the winner.

Q5: How does Social Security factor into this decision?

A: This is an advanced but critical point. Your “provisional income” (which includes your Traditional IRA withdrawals) determines how much of your Social Security benefits are taxable. By having a source of tax-free income from a Roth, you can lower your provisional income, potentially reducing the taxability of your Social Security benefits. This is another powerful argument for tax diversification.

Conclusion: Building Your Tax-Adaptive Retirement

The Roth vs. Traditional question doesn’t have a one-size-fits-all answer, but it does have a strategically optimal one for your specific situation.

Stop thinking of it as a permanent, binary choice. Instead, view it as an ongoing strategic decision. Your goal is to build a retirement fund that is adaptive to the tax landscape of your future.

- Use Traditional accounts to capture high-value tax deductions during your peak earning years and to efficiently fill lower tax brackets in retirement.

- Use Roth accounts to lock in low tax rates early in your career, to effectively save more past contribution limits, to gain unparalleled flexibility, and to create a tax-free pool of money for large expenses and legacy goals.

For most people, the ultimate victory lies not in choosing one over the other, but in skillfully building and using both. By understanding the core principles outlined in this guide, you can move forward with confidence, making annual contributions that are not just about saving money, but about saving smartly for a secure and tax-efficient future.