Executive Summary

The American retail landscape is in the midst of a profound transformation, driven by the relentless ascent of Direct-to-Consumer (DTC) brands. This shift represents more than a change in distribution channels; it is a fundamental reimagining of the brand-consumer relationship. By eschewing traditional wholesale intermediaries and selling directly to customers, digitally-native vertical brands (DNVBs) like Warby Parker, Glossier, and Dollar Shave Club have upended decades-old industry paradigms. This deep-dive analysis explores the convergence of technological, cultural, and economic forces that fueled the DTC boom. It dissects the core pillars of the DTC playbook—from data-centricity and brand storytelling to community building—and provides a critical examination of the formidable challenges these brands now face as the model matures. The report concludes that the future of DTC is not about a pure-play digital existence, but a resilient, omnichannel evolution where the direct relationship remains the most valuable asset. For legacy retailers and new entrants alike, understanding this disruption is no longer optional—it is essential for survival.

1. Introduction: The Quiet Revolution

The year is 2010. A man in a blue shirt stands in front of a plain background and, with deadpan humor, demonstrates the absurdity of spending $20 on razor blades. With a budget of $4,500, the video for Dollar Shave Club goes viral, garnering millions of views in days and signaling the start of a retail revolution. Around the same time, a group of Wharton students frustrated by the high cost of eyeglasses launches Warby Parker, offering stylish, prescription-grade glasses for a fraction of the price, shipped directly to customers’ homes.

These were not merely new companies; they were the vanguard of a new business model: Direct-to-Consumer (DTC).

Also known as Digitally-Native Vertical Brands (DNVBs), these companies are defined by their operational structure: they control the design, marketing, sales, and customer experience of their products, bypassing traditional retail intermediaries like department stores, big-box chains, and distributors. This report provides a comprehensive analysis of the DTC phenomenon in the United States. We will explore its origins, its core strategic advantages, the formidable challenges it now faces, and its evolving future in an increasingly crowded and complex retail ecosystem.

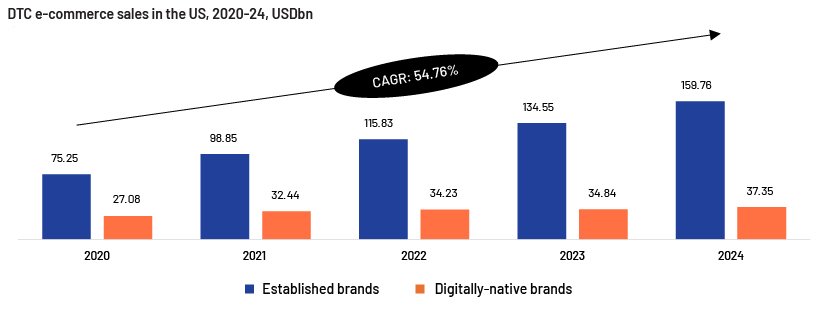

2. The Perfect Storm: Conditions Fueling the DTC Boom

The rise of DTC was not an accident. It was the result of a unique convergence of enabling technologies and shifting consumer behaviors that created a “perfect storm” for disruption.

2.1 The Technological Enablers

- The Proliferation of E-commerce Platforms: The maturation of robust, scalable, and user-friendly platforms like Shopify, BigCommerce, and Magento democratized online retail. A brand no longer needed a multi-million dollar IT budget to build a beautiful, functional e-commerce store. This lowered the barrier to entry dramatically.

- The Social Media Advertising Engine: The rise of Facebook and Instagram provided an unprecedentedly targeted and measurable advertising channel. DTC brands could use rich demographic, psychographic, and behavioral data to reach their ideal customer profile with surgical precision, turning social feeds into the new storefront.

- The Logistics and Fulfillment Revolution: The infrastructure built by Amazon and the growth of sophisticated third-party logistics (3PL) providers like ShipBob and Deliverr made efficient, affordable, and fast fulfillment accessible to small brands. Customers now expect two-day shipping as standard, an expectation DTC brands could meet without building their own warehouses from scratch.

- The Data Analytics Advantage: Cloud-based analytics tools allowed DTC brands to track every click, hover, and purchase. This data became their lifeblood, enabling a cycle of continuous optimization of their website, marketing campaigns, and even product development.

2.2 The Shifting Consumer Psyche

- The Demand for Authenticity and Story: Millennials and Gen Z, the core demographics for early DTC success, developed a deep skepticism of traditional, polished corporate advertising. They craved authentic connection, transparency, and brands with a compelling mission or story. DTC brands excelled at this narrative-driven marketing.

- The Value of Convenience and Experience: The DTC model was built for convenience—products delivered to your door, easy returns, and a seamless digital experience. This aligned perfectly with the growing consumer preference for saving time and effort.

- The Search for Personalization: Consumers grew tired of the one-size-fits-all approach of mass-market brands. DTC companies leveraged their direct relationship to offer personalized products, recommendations, and communication, making the customer feel uniquely understood.

3. Deconstructing the DTC Playbook: The Pillars of Disruption

The success of leading DTC brands can be attributed to a disciplined execution of a core strategic playbook.

3.1 Owning the Customer Relationship: The Ultimate Asset

This is the single most important advantage of the DTC model. By interacting with customers directly, brands gain:

- First-Party Data: They own the data on who their customers are, what they buy, and how they behave. This is invaluable for personalization, forecasting, and building a defensible moat, especially in a world of increasing data privacy regulation (like iOS updates limiting tracking).

- Control of the Brand Narrative: There is no retail partner to misplace products or provide poor service. The brand controls every touchpoint, from the unboxing experience to customer support emails, ensuring a consistent and premium brand image.

- Higher Lifetime Value (LTV): A direct relationship allows for ongoing engagement through email marketing, loyalty programs, and community building, encouraging repeat purchases and increasing the customer’s lifetime value.

3.2 The Power of Vertical Integration and Margin Control

The traditional retail model involves multiple markups. A manufacturer sells to a wholesaler, who sells to a retailer, each adding their own margin. The DTC model collapses this chain.

- Improved Unit Economics: By cutting out the middlemen, DTC brands can capture the margin that would have gone to retailers. This allows them to offer a higher-quality product at a similar price point or a similar product at a significantly lower price, creating a powerful value proposition (as seen with Warby Parker and Dollar Shave Club).

- Agility and Speed: Controlling the entire supply chain, from design to delivery, allows for faster iteration. They can test new products, designs, and features with their audience and quickly scale what works, a process far more agile than that of legacy brands reliant on seasonal retail buy-in.

Read more: The 90+ Rule of Retirement: Planning for a Longer Future

3.3 Brand as a Story, Product as a Solution

DTC brands are master storytellers. They don’t just sell products; they sell an identity, a solution to a problem, and a sense of belonging.

- Mission-Driven Marketing: Many DTC brands are built around a clear, disruptive mission. Allbirds is about sustainable materials. Hims & Hers is about destigmatizing telehealth. This mission creates an emotional hook that transcends the product itself.

- Content-First Approach: They invest heavily in high-quality content—blogs, videos, social media posts—that provides value to their audience beyond a simple sales pitch. A skincare brand becomes a source of dermatological advice; a fitness brand becomes a hub for workout tutorials.

3.4 Community as a Moat

The most successful DTC brands have cultivated passionate communities that act as a powerful, self-sustaining marketing engine.

- User-Generated Content (UGC): Brands like Glossier famously built their product line and marketing almost entirely by listening to and featuring their community. Customers posting photos with their products become a more trusted form of advertising than any corporate campaign.

- Creating Brand Advocates: A strong community turns customers into vocal advocates who defend the brand and recruit new members, effectively lowering customer acquisition costs (CAC) and creating a durable competitive advantage.

4. The Pendulum Swings: The Maturing Market and Mounting Challenges

The initial wave of DTC was characterized by euphoric growth and venture capital funding. However, as the market has matured, a series of formidable challenges have emerged, forcing a strategic pivot.

4.1 The Customer Acquisition Cost (CAC) Crisis

The very engine that powered DTC growth—targeted social media advertising—has become its biggest headache.

- Platform Saturation: The digital advertising space is now incredibly crowded. Every brand is competing for attention on the same few platforms, driving up auction prices.

- The Privacy Crackdown: Apple’s App Tracking Transparency (ATT) framework has severely limited the ability of advertisers to track users across apps and websites. This has blunted the precision of Facebook’s targeting, making ads less effective and more expensive.

- The Result: Customer Acquisition Costs have skyrocketed for many DTC brands, eroding their hard-won margin advantages and making profitable growth increasingly difficult.

4.2 The Scaling Imperative and the “CAC to LTV” Ratio

Venture-backed DTC brands are under immense pressure to grow rapidly. This often leads to a focus on top-line revenue at the expense of profitability. The key metric, the LTV to CAC ratio (the lifetime value of a customer versus the cost to acquire them), has become unsustainable for many. A ratio of 3:1 is considered healthy, but many public DTC companies have seen this ratio compress toward 1:1, a path to eventual failure.

4.3 The Logistics and Operational Reality

Managing the entire supply chain is complex and capital-intensive. As brands scale, they face challenges with:

- Inventory Management: Predicting demand accurately to avoid being either out-of-stock or stuck with dead inventory.

- Returns Processing: The “hassle-free returns” policy that wins customers is a major operational and financial burden, especially for categories like apparel where return rates can exceed 30%.

- Global Expansion: Navigating international shipping, tariffs, and compliance adds another layer of complexity.

4.4 The Legacy Counter-Attack

Legacy retailers are not standing still. They have responded aggressively by:

- Launching Their Own DTC Channels: Nike has made a strategic pivot to focus on its own app and SNKRS platform, while simultaneously reducing its reliance on wholesale partners like Foot Locker.

- Acquiring DTC Brands: Unilever bought Dollar Shave Club; Procter & Gamble acquired Billie. This allows incumbents to buy innovation and a direct channel.

- Improving Their Own E-commerce: Big-box retailers like Walmart and Target have invested billions in their online platforms, leveraging their vast physical store networks for omnichannel services like BOPIS (Buy Online, Pick Up In-Store), which pure-play DTC brands cannot initially match.

Read more: Retirement Planning in 2025: What You Need to Know

5. The Next Chapter: The Evolution of the DTC Model

In response to these headwinds, the DTC model is evolving. The future is not “digital-only” but “direct-relationship-first.”

5.1 The Strategic Pivot to Physical Retail

Contrary to initial dogma, leading DTC brands are increasingly opening physical stores. However, these are not traditional stores; they are brand experience centers.

- Experiential Showrooms: Casper’s “Dreamery” allows you to nap in a pod. Glossier’s stores are designed as Instagram-worthy destinations with floral installations and a community vibe. The goal is not just to move inventory, but to deepen brand connection and provide a tangible experience that can’t be replicated online.

- Lowering CAC: A physical storefront serves as a permanent billboard and can acquire customers at a fixed cost, providing a hedge against rising digital ad prices.

5.2 The Omnichannel Imperative

The winning strategy is to be wherever the customer is. This means a seamless integration of digital and physical touchpoints.

- Buy Online, Pick Up In-Store (BOPIS): Warby Parker excels at this, allowing customers to reserve frames online and try them on in-store.

- In-Store Returns for Online Orders: This convenience enhances the customer experience and drives foot traffic.

5.3 Selective Wholesale and Partnerships

In a strategic twist, some DTC brands are now selectively partnering with wholesale retailers. This “if you can’t beat ’em, join ’em” approach provides access to new customer segments and massive scale.

- Examples: Allbirds now sells in Nordstrom. Native deodorant is available at Target. This provides a powerful brand-awareness boost and can be a more efficient customer acquisition channel than expensive digital ads, though it requires ceding some margin and control.

5.4 Product and Category Expansion

To increase customer LTV, successful DTC brands are expanding beyond their initial hero product.

- The “Platform” Strategy: Harry’s razors expanded into shaving cream, then body wash, then deodorant, aiming to become a full male grooming platform. This increases the share of wallet from each acquired customer.

6. Conclusion: The End of the Beginning

The initial, disruptive wave of pure-play DTC is over. The model has not failed; it has matured. The core tenets—owning the customer relationship, leveraging data, and building a authentic brand story—are now permanent features of the modern retail landscape.

The DTC revolution proved that a brand built on a direct, value-driven relationship with the consumer could not only compete with but defeat entrenched industry giants. However, the next chapter will be defined by a more pragmatic, omnichannel approach. The winners will be those who can blend the digital agility and storytelling prowess of a DTC native with the operational scale, logistical prowess, and physical presence of a traditional retailer. The disruption is not ending; it is evolving, and its lessons are now mandatory for anyone in the business of building a brand in the 21st century.

FAQ Section

Q1: What is the fundamental difference between a DTC brand and a traditional brand that also sells on its website?

The difference is structural and strategic. A traditional brand like Nike or Procter & Gamble was built on a wholesale model, relying primarily on retailers to reach customers. They added e-commerce as a supplementary channel. A true DTC brand is built from the ground up to bypass retailers entirely. The direct channel is its primary, and often initial, route to market. It controls its entire supply chain and, most importantly, owns the one-to-one relationship with its customer.

Q2: Why are so many DTC brands struggling or being acquired now?

Many are facing a “profitability cliff.” They were able to achieve initial growth by spending heavily on digital advertising when it was cheap and effective. As discussed, rising Customer Acquisition Costs (CAC) due to platform saturation and privacy changes have eroded their margins. Many were operating with unsustainable LTV:CAC ratios, relying on venture capital to fund losses. When growth slows or funding becomes scarce, they are forced to either sell to a larger entity that can provide scale (like a Unilever) or face collapse.

Q3: Isn’t the move into physical stores and wholesale a betrayal of the DTC model?

It’s better viewed as an evolution. The core of the DTC model is not “digital-only”; it’s “direct relationship-first.” A physical store owned by the brand is another form of a direct channel—it’s a controlled environment to interact with the customer. Selective wholesale is a strategic calculation: by trading some margin for massive scale and awareness, a brand can acquire new customers it couldn’t reach affordably online, with the goal of eventually moving them into its higher-margin direct channels (e.g., through loyalty programs promoted on the packaging sold at Target).

Q4: Can a new DTC brand still succeed in today’s crowded market?

Yes, but the playbook has changed. It is no longer enough to have a great product and run Facebook ads. Success requires:

- A highly specific niche: Don’t try to be the next “everything apparel” brand. Find a passionate, underserved community.

- A unique brand story and authentic community building from day one.

- A diversified marketing strategy that relies less on paid ads and more on organic social, SEO, content marketing, and strategic partnerships.

- A ruthless focus on unit economics and profitability from the start, rather than a “growth at all costs” mentality.

Q5: What is the biggest long-term advantage a DTC brand has over a traditional competitor?

Ownership of the customer relationship and the first-party data that comes with it. In an era where third-party data is becoming less accessible, the deep, direct understanding of who your customers are, what they want, and how they behave is an invaluable asset. It allows for superior product development, personalized marketing, and the building of a loyal community that acts as a durable competitive moat.

Disclaimer: This market analysis is based on current data, public filings, and industry trends as of 2024. The retail landscape is dynamic, and the performance of individual companies may vary. This report is intended for informational and strategic purposes and should not be considered financial advice.

Read more: AI for Trading: The 2025 Complete Guide