Summary

Tax-efficient investing enables American investors to maximize after-tax returns by strategically managing accounts, asset allocation, and portfolio turnover. Leveraging retirement accounts, municipal bonds, ETFs, and tax-loss harvesting reduces tax liabilities while growing wealth. This guide provides actionable tips, real-life examples, and practical strategies to achieve smarter, tax-savvy investing in the U.S. market.

Introduction: Why Tax Efficiency Matters

Taxes are often the largest unseen cost for investors. Two portfolios with identical market returns can yield drastically different results after taxes. For instance, a 30-year-old investing $10,000 annually at 7% returns could lose nearly $100,000 in taxes over three decades if no tax-efficient strategies are applied.

Real-Life Example:

Consider two investors with identical $10,000 annual contributions. Investor A holds all assets in a taxable brokerage account, while Investor B allocates across a Roth IRA, 401(k), and municipal bonds. Over 30 years, Investor B’s portfolio can outperform by 20–30% due to tax savings and compounding.

In 2025, tax-efficient investing is especially critical due to rising income brackets, changing capital gains rates, and evolving U.S. tax policies.

1. Understanding Tax-Efficient Investing

Tax-efficient investing focuses on maximizing after-tax returns rather than just pre-tax performance. The goal is to reduce tax drag on your portfolio while still achieving growth.

Key Principles

- Asset location: Place tax-inefficient investments in tax-advantaged accounts

- Capital gains management: Time sales to minimize taxable gains

- Dividend planning: Favor qualified dividends over non-qualified for lower tax rates

- Portfolio turnover control: Avoid excessive trading that triggers taxable events

Insight:

High-income Americans benefit from municipal bonds and Roth IRA allocations, while moderate earners may optimize with long-term capital gains strategies and tax-deferred accounts.

2. Leverage Tax-Advantaged Accounts

A. 401(k) and 403(b) Plans

- Contributions are pre-tax, lowering current taxable income

- Employer matching adds immediate return

- Taxes are deferred until withdrawal

Example:

Contributing $20,000 to a 401(k) while in the 24% tax bracket reduces taxable income by nearly $5,000. Over time, this reduces the total tax burden while growing investments.

B. Individual Retirement Accounts (IRA)

- Traditional IRA: Contributions may be tax-deductible; withdrawals are taxed

- Roth IRA: Contributions are after-tax; withdrawals are tax-free

- Backdoor Roth IRA: Useful for high-income earners exceeding standard contribution limits

C. Health Savings Accounts (HSA)

- Triple tax benefit: deductible contributions, tax-free growth, and tax-free withdrawals for qualified medical expenses

- Can act as a supplemental retirement account

Real-Life Insight:

A 35-year-old investing $3,500 annually in an HSA could accumulate over $100,000 by age 65 with tax-free growth, assuming moderate returns.

3. Choosing Tax-Efficient Investments

Investment selection plays a critical role in minimizing tax impact.

A. Municipal Bonds (Munis)

- Interest is generally federally tax-free and sometimes state-tax-free

- Ideal for high-income investors seeking predictable income

B. Exchange-Traded Funds (ETFs)

- ETFs are inherently tax-efficient due to in-kind creation/redemption processes

- Minimize capital gains distributions

C. Index Funds

- Passive management reduces turnover

- Lower short-term capital gains exposure

D. Individual Stocks

- Favor long-term holdings (>1 year) to take advantage of lower capital gains rates

Example:

Holding Apple or Microsoft for over a year instead of frequent trades can cut federal tax rates from 37% to 15–20% on gains.

4. Tax-Loss Harvesting

Definition: Selling underperforming investments to offset capital gains.

Example:

- Sell $5,000 of losing stock to offset $5,000 of gains

- Net taxable gain becomes $0

- Excess losses can be carried forward indefinitely

Tip: Avoid the wash-sale rule, which disallows the deduction if you repurchase the same security within 30 days.

5. Asset Location Strategy

Placing investments in the right accounts maximizes tax efficiency:

| Asset Type | Best Account Type | Reason |

|---|---|---|

| Taxable bonds | 401(k)/IRA | Interest taxed as ordinary income |

| Municipal bonds | Taxable | Already tax-exempt |

| Growth stocks | Roth IRA or taxable | Capital gains tax advantages |

| REITs | 401(k)/IRA | Dividends taxed at ordinary rates |

Example:

Holding REIT ETFs in a 401(k) avoids high-tax ordinary income, while municipal bonds in taxable accounts provide tax-free income.

6. Managing Capital Gains and Dividends

A. Long-Term vs Short-Term Gains

- Short-term (<1 year): Ordinary income tax rates (up to 37%)

- Long-term (>1 year): Preferential rates (0%, 15%, 20%)

B. Qualified vs Non-Qualified Dividends

- Qualified dividends taxed at long-term capital gains rates

- Non-qualified dividends taxed at ordinary income rates

Example:

$10,000 in qualified dividends could save $1,500–$2,000 annually compared to non-qualified dividends.

7. Retirement Account Strategies

- Max out employer 401(k) match first

- Use Roth conversion ladders in lower-income years

- Maintain a mix of Roth, Traditional, and taxable accounts for withdrawal flexibility

Example:

A 50-year-old converts $50,000 from a Traditional IRA to Roth IRA gradually to reduce tax liability in retirement.

8. Diversifying for Tax Efficiency

Diversification is not just risk management—it’s a tax tool.

- Mix taxable, tax-deferred, and tax-free accounts

- Include stocks, bonds, and alternatives

- Monitor dividend yield and turnover to reduce tax drag

Case Study:

Investor A: all assets taxable, 6% after-tax returns.

Investor B: mix of Roth IRA, 401(k), taxable, 8% after-tax returns over 10 years.

9. Using Real Estate and REITs for Tax Advantages

- Real estate offers depreciation deductions

- REITs in tax-advantaged accounts avoid ordinary income taxes

- 1031 exchanges defer capital gains when swapping properties

Example:

Rental property depreciation of $20,000 can significantly reduce taxable income annually.

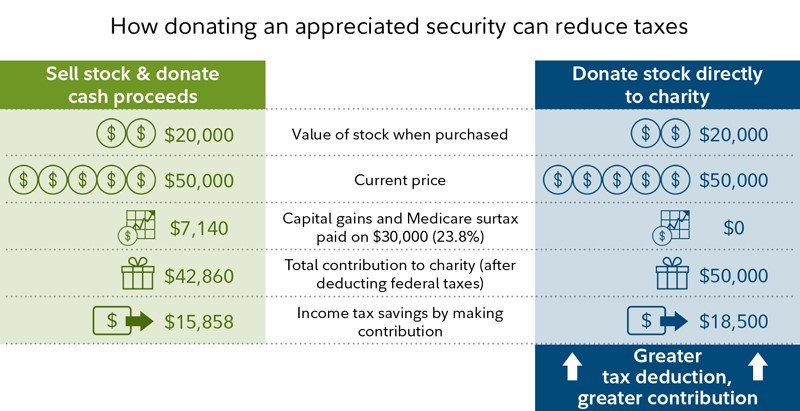

10. Charitable Giving and Tax Planning

- Donate appreciated stock to avoid capital gains taxes

- Use Donor-Advised Funds (DAFs) for flexibility and deduction timing

- Integrate charitable contributions with retirement withdrawals

Example:

Donate $10,000 in stock with $5,000 cost basis to avoid taxes on gains while deducting $10,000 from income.

11. Tax-Efficient Withdrawal Strategies

- Withdraw from taxable accounts first

- Convert to Roth in low-income years

- Plan around RMDs to avoid penalties

Example:

A retiree withdraws from taxable accounts initially, delaying Roth withdrawals to manage tax exposure and reduce RMD impact.

12. Monitoring Legislation and Policy Changes

Key 2025 trends:

- Capital gains rate adjustments

- Estate and gift tax exemptions

- Deduction changes for retirement contributions

Tip: Consult a tax advisor annually to adjust strategies according to policy updates.

13. Tools and Resources for Tax-Efficient Investing

- Brokerage Platforms: Vanguard, Fidelity, Schwab

- Robo-Advisors: Betterment, Wealthfront (tax-loss harvesting automation)

- Tax Software: TurboTax, H&R Block

- Research: IRS publications, Morningstar tax reports

14. Case Study: A Tax-Efficient Portfolio in Action

Scenario: $100,000 Investment Allocation

| Asset | Account Type | Expected Tax Impact |

|---|---|---|

| S&P 500 ETF | Roth IRA | Tax-free growth |

| Municipal Bonds | Taxable | Interest tax-exempt |

| REIT ETF | 401(k) | Tax-deferred |

| Gold ETF | Taxable | Long-term gains |

Outcome:

Combining tax-free growth, tax-deferred income, and taxable assets with favorable treatment reduces annual tax liability while maintaining diversification.

15. Frequently Asked Questions (FAQs)

1. What is tax-efficient investing?

Tax-efficient investing focuses on maximizing after-tax returns by choosing accounts, assets, and strategies that minimize taxes over time. It’s not about avoiding taxes but strategically planning to pay less legally, leveraging retirement accounts, municipal bonds, ETFs, and long-term holdings to increase net wealth.

2. How can I reduce capital gains taxes?

Hold investments for more than one year to qualify for long-term capital gains rates. Use tax-loss harvesting to offset gains and consider municipal bonds for tax-exempt interest. Timing sales and strategic account placement further reduce capital gains exposure.

3. Should I prioritize Roth or Traditional accounts?

Roth accounts provide tax-free growth, ideal for young investors or high-growth portfolios. Traditional accounts offer immediate tax deductions, suitable for high-income earners. Combining both types allows flexibility in retirement withdrawals and tax planning.

4. Are ETFs more tax-efficient than mutual funds?

Yes, ETFs generally trigger fewer capital gains due to the in-kind creation/redemption mechanism, whereas actively managed mutual funds often distribute gains annually, creating a higher tax burden.

5. What is a backdoor Roth IRA?

It’s a strategy for high-income earners to contribute to a Roth IRA by first contributing to a Traditional IRA and then converting it to a Roth, bypassing standard income limits. It allows tax-free growth in retirement.

6. How does dividend type affect taxes?

Qualified dividends are taxed at long-term capital gains rates, usually lower than ordinary income. Non-qualified dividends are taxed at your regular income rate, making qualified dividends more tax-efficient.

7. What are the tax benefits of municipal bonds?

Interest from municipal bonds is often federal tax-exempt and sometimes state tax-exempt, making them ideal for high-income investors seeking safe, income-generating assets.

8. How can real estate reduce taxes?

Depreciation on investment property reduces taxable income. Additionally, 1031 exchanges defer capital gains when swapping properties, providing tax deferral while growing a real estate portfolio.

9. How does tax-efficient investing affect retirement planning?

It increases after-tax wealth, allowing more spending or reinvestment in retirement. Tax-efficient strategies like Roth conversions, tax-loss harvesting, and account diversification ensure a smoother, less taxable income stream.

10. How often should I review tax-efficient strategies?

Annually, or whenever there are major life changes, income shifts, or tax law updates. Regular reviews ensure your portfolio remains optimized and compliant with current U.S. tax laws.

16. Conclusion

Tax-efficient investing is critical for American investors aiming to maximize wealth. By strategically using tax-advantaged accounts, municipal bonds, ETFs, and portfolio management techniques like tax-loss harvesting and asset location, investors can significantly reduce tax liabilities.

The key is a holistic approach: combining investment diversification, long-term planning, and awareness of policy changes. Smart tax strategies don’t just save money—they compound wealth over time, ensuring financial security for decades.

Read this also : https://fazi.world/navigating-the-app-economy-a-guide-to-investing-in-us-tech-stocks-and-etfs/